5 Things That Actually Drive Your Roofing Company's Sale Price (and 3 That Don't)

Your roofing company's sale price comes down to one question a buyer is always asking: how much money will this business make me, and how confident...

Selling a logistics company in Tennessee requires proof that cash flow, contracts, fleet condition, and compliance can withstand buyer and lender review. The real constraint is not the buyer's interest. It is whether the business can survive diligence without price cuts, financing issues, or avoidable closing delays.

This matters even more in the logistics industry, as buyers are quite selective about risk and transferability. PMCF reported 131 closed U.S. transportation and logistics M&A transactions in the trailing twelve months ending Q3 2025, which shows deals are still getting done. However, that's only true for businesses that present clean financials, credible operations, and defensible value.

If you are thinking about selling a logistics business, the right preparation starts well before a confidential information memorandum is drafted.

This guide covers

P.S. Before you take your transportation company to the market, it helps to know whether the financials, fleet files, and transfer issues will stand up under buyer review. At Legacy Entrepreneurs, we help Tennessee business owners evaluate sale readiness and price support through our business valuation services and brokerage support.

Request a business valuation to identify the issues most likely to affect buyer confidence, financing, and closing before they reduce leverage.

Selling a logistics company in Tennessee starts with proving that the business can hold together under new ownership. A serious buyer will test whether cash flow is dependable, whether customer relationships are likely to continue, whether fleet and compliance records point to future problems, and whether the business can keep performing without the seller at the center of daily operations.

That is why the sale process should begin with records, cleanup, and positioning, not with a rule-of-thumb valuation. The stronger the evidence behind the business, the easier it is to support price and terms once due diligence begins.

Before you try to sell your logistics business, determine whether the company is actually ready for sale. A logistics business can produce strong revenue and still be difficult to sell if dispatch lives in the owner’s phone, top accounts are tied to informal client relationships, fleet records are incomplete, or profitability swings too sharply from month to month.

A sellability review should focus on transfer risk. That includes customer concentration, recurring revenue, management team depth, owner dependence, contract terms, fleet ownership, safety records, claims history, working capital needs, and whether the company’s ability to win and retain freight depends too heavily on the seller personally.

This review matters because many business owners start by asking how to maximize the sale price before they understand what could reduce it. In the logistics industry, weak retention rates, thin margins, inconsistent reporting, poor fleet maintenance, or undocumented compliance problems often matter more than a broad market value estimate.

A buyer does not buy a logistics business based on revenue alone. Buyers are looking at whether earnings are likely to hold after closing, how exposed the company is to customer loss or insurance pressure, and whether the operating model can transfer cleanly to new ownership. That is why two logistics companies with similar annual revenues can attract very different offers.

A strong buyer will compare these files against the story presented in the CIM and management conversations. If the evidence does not support the claims, buyers see risk, not upside.

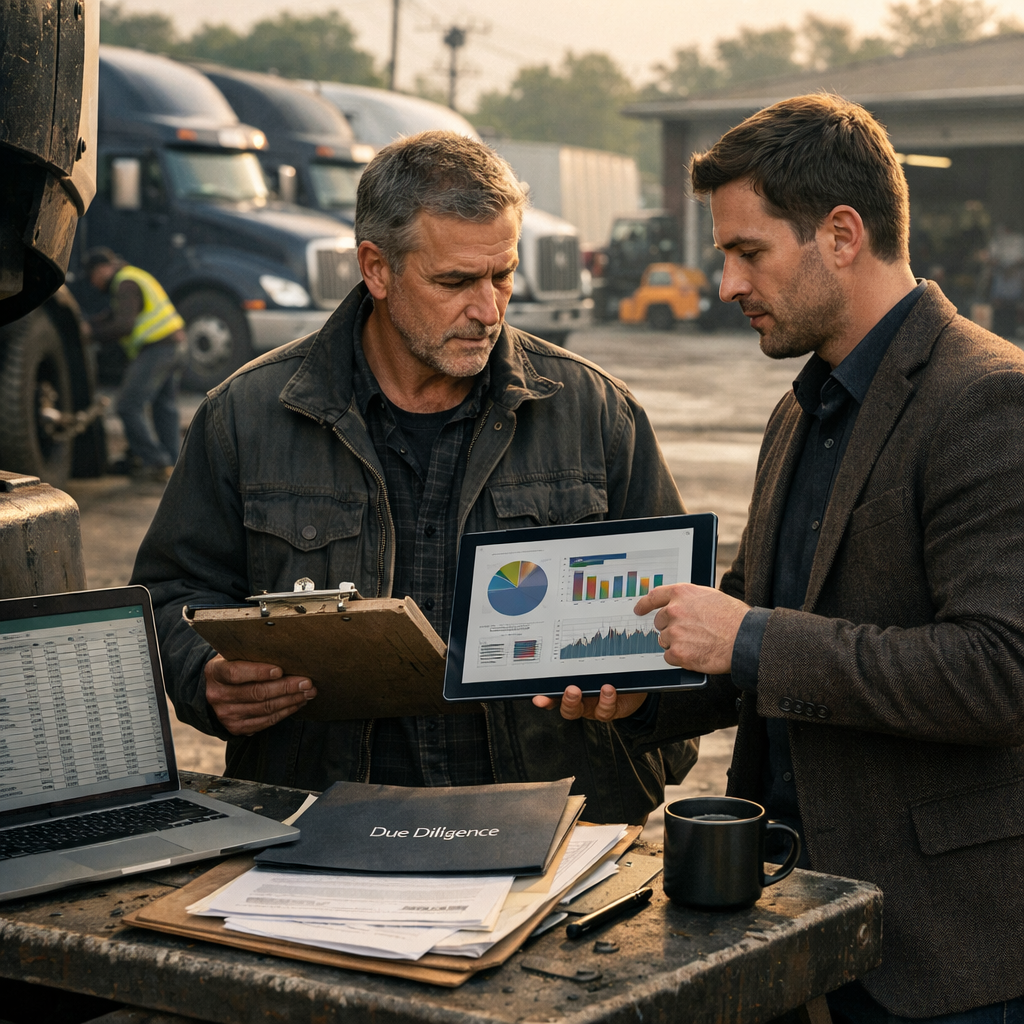

Financial cleanup matters because buyers and lenders will compare internal statements to tax returns, debt schedules, payroll records, fleet files, and operating reports. If those records do not line up, confidence in the value of your business falls quickly.

Three Years Of Filed Tax Returns: Include complete filed returns that align with internal profit and loss statements so the buyer can confirm revenue, profitability, depreciation, officer compensation, and major expense categories. If returns do not tie back to internal books, the buyer will question the quality of earnings and may lower the price for your business.

Monthly Profit And Loss Statements: Prepare at least 36 months of monthly P&Ls plus a trailing twelve-month view that explains swings in freight demand, fuel expense, repairs, labor, or unusual customer volume. Buyers use this to judge predictability and whether recent performance is expected to continue.

Balance Sheets and Debt Schedules: Provide monthly balance sheets, loan schedules, equipment notes, and credit facility detail so the buyer can evaluate working capital, leverage, and which liabilities need payoff at closing. Missing debt detail often creates problems around net proceeds and lien releases.

Revenue By Customer And Service Line: Break out revenue by top accounts and by service type, such as trucking, freight brokerage, freight forwarding, or third-party logistics. This helps buyers evaluate concentration risk, margin mix, and opportunities for growth.

Add-Back Support: Document every seller's add-back with invoices, payroll records, or clear explanations. Personal expenses, one-time legal costs, or unusual owner compensation can support valuation only if they are real, non-recurring, and provable.

Payroll and Headcount Detail: Include compensation by role, contractor versus employee status, and overtime patterns where relevant. Buyers are looking for labor dependency, management gaps, and whether the payroll structure matches the operating model presented.

Read Next: Bad Bookkeeping Kills Deals — Focus on These 4 Fixes

A logistics company becomes more valuable when the buyer sees a business, not a job that happens to generate revenue. If the seller still owns the dispatch relationships, handles the key customers, approves every exception, and resolves every service issue personally, the company’s ability to transfer is limited. Buyers see that immediately.

This matters because buyer confidence depends on continuity after closing. A business with a credible management team, documented workflows, and clear responsibility across dispatch, operations, sales, and customer service can command stronger interest. The buyer can picture new ownership stepping in without major disruption.

If owner dependency is still high, preparation should focus on practical delegation. That may include moving key accounts to account managers, documenting dispatch procedures, clarifying how after-hours issues are handled, and deciding whether the business needs stronger operational leadership. In some cases, adding or strengthening a manager before sale improves transferability and helps maximize valuation because buyers are paying for continuity, not personal heroics by the seller.

Read Next: Should You Hire a Manager or a Sales Leader? 6 Real Scenarios That Show the Right Move

Different buyers evaluate the same logistics business differently. Strategic buyers may focus on network fit, customer overlap, service-line expansion, or whether the company helps them strengthen their supply chain position in Tennessee or a neighboring market. Some are interested in expanding through a merger or tuck-in acquisition.

Private equity may focus more on management team quality, growth potential, scalability, and whether the business fits a broader roll-up strategy. An individual buyer may care more about financing, simplicity, and how much transition support is required.

This matters because the best outcome does not always come from the broadest list of potential buyers. Some buyers understand brokerage, third-party logistics, or freight forwarding economics better than others. Some will value trucking companies and asset-heavy operations more accurately because they have the knowledge and experience to evaluate fleet risk, insurance pressure, and Department of Transportation compliance. Others will discount the business heavily if they do not understand the model.

A business broker can help position the company with the buyers most likely to value its contracts, revenue streams, management team, and competitive advantage correctly. That does not guarantee you get the highest headline number, but it improves the odds of getting price and terms that hold through due diligence.

Read Next: Why Work with a Nashville Business Broker?

A serious buyer expects the sales materials to answer hard questions before management meetings begin. That does not mean oversharing early. It means presenting the logistics business with enough evidence to build confidence.

Read Next: Why a Strong Confidential Information Memorandum is Key to a Successful Business Sale

The sale process becomes more fragile after the LOI, not less. An attractive headline number can still produce a weak deal if exclusivity runs too long, working capital is undefined, or the buyer has too much room to renegotiate after diligence.

A disciplined LOI should spell out the main price and terms clearly enough to reduce later ambiguity. That includes whether any part of the purchase price is contingent, whether seller financing is required, what assets and liabilities are included, whether employment or transition support is expected, and how long exclusivity lasts. In a logistics acquisition, the buyer may also focus early on contract assignment, claims history, lien payoff, key employee retention, and whether any part of the purchase price will be held back.

Once due diligence starts, speed and consistency matter. If requests for safety records, insurance files, customer contracts, fleet schedules, financial support, and compliance documents are answered slowly or inconsistently, buyer confidence drops. That often leads to pressure on deal terms, not just more questions.

This is also where financing matters. SBA 7(a) loans can be used for changes of ownership, which is one reason lenders reviewing a smaller transaction will look closely at cash flow support, working capital, and the company’s ability to keep performing after closing.

A controlled diligence process protects sale proceeds, reduces re-trade risk, and gives the seller a better chance to sell their business on terms that hold together through closing.

When selling a logistics company in Tennessee, transfer and compliance issues can affect price, financing, and timing, even when the business has strong revenue and cash flow. These issues affect whether the buyer believes the business can keep operating cleanly under new ownership and whether the sale process can move without late surprises.

If the logistics business operates as a motor carrier, broker, or freight forwarder, registration and authority records should be reviewed before the company goes to market. The buyer will want to know which records sit with the selling entity, which changes or notices may be required after closing, and whether the company’s registrations match how it actually operates.

That review matters because FMCSA does not treat every registration item the same way. FMCSA says USDOT numbers are not transferable. It also says the agency will record and track an Operating Authority transfer when the transfer is part of a purchase transaction involving an entire operation and both parties provide adequate notice documenting the transaction. FMCSA also requires certain ownership, legal-name, or registration changes to be updated through its registration process.

If the buyer cannot confirm that these records will remain in order through closing and transition, the issue can slow closing, add conditions to the deal, or increase the amount of seller support needed after the sale.

Titles, Liens, UCC Filings, And Equipment Transfer Readiness

Title and lien problems can slow a logistics sale even when the buyer is still interested in the business. When selling your transportation company, you have to ensure the transfer package shows who owns each revenue-producing asset, what debt is attached to it, whether any lender has a filed security interest, and whether leased equipment can stay in service after closing.

Buyers are not asking for this information out of caution alone. They need to confirm which trucks, trailers, and other operating assets are actually being transferred, what must be paid off at closing, and whether any consent, release, or updated documentation will be required before the business can keep operating under new ownership.

Vehicle Titles: Confirm that each truck, trailer, and other titled unit is in the selling entity’s legal name, not the owner’s personal name or an affiliated company’s name. Match the title record to the fleet schedule, VIN, unit number, lienholder, and insurance schedule. If the title, lender record, and insurance file do not match, transfer problems often surface late in diligence or at closing.

Lien Payoff Support: Pull current payoff letters for each financed truck, trailer, tractor, chassis, forklift, or other financed equipment included in the sale. The file should show the lender name, account number, payoff amount, per diem if applicable, and instructions for release of lien once funds are received. Buyers and lenders use this to confirm how much debt must be cleared from the sale proceeds and whether the release timing could delay closing.

UCC Filings: Run a UCC search against the selling entity and identify blanket liens, equipment-specific filings, old lender filings that were never terminated, and any filing that appears to cover accounts receivable, inventory, equipment, deposit accounts, or general intangibles. This matters because a filing may affect more than one truck note. It can also cover broad categories of business assets and create release issues if it is not cleaned up before closing. Tennessee’s Secretary of State describes UCC filings as public notice of a creditor’s security interest in collateral.

Leased Equipment Schedules: Separate leased assets from owned assets and gather the actual lease schedules for tractors, trailers, forklifts, warehouse equipment, or office equipment that matters to operations. Review assignment restrictions, buyout terms, return conditions, end-of-term dates, mileage limits where relevant, and whether the buyer will need the lessor’s consent or a replacement lease.

Asset Inclusion List: Build a closing schedule that identifies exactly which trucks, trailers, forklifts, telematics units, shop equipment, spare engines, leased units, and other operating assets are included or excluded. Also, identify excluded cash, excluded personal vehicles, and any equipment the seller plans to keep. Ambiguity here often turns into renegotiation because the buyer is pricing the company based in part on the assets needed to keep serving freight customers after closing.

Insurance and safety records matter because they show operating risk that may not be obvious from the income statement alone. A logistics business can report solid EBITDA while still carrying claim patterns, insurance pressure, or FMCSA-related issues that change how a buyer evaluates future profitability.

Tennessee's market position can affect how strategic buyers evaluate an acquisition. A logistics business with established customer relationships, repeat customer demand, and a location that supports how the company operates may attract more interest than a business with similar revenue but a weaker regional position. Buyers who might be interested in expanding across Nashville, Middle Tennessee, or nearby freight corridors will look at whether the customer base, revenue streams, and service footprint fit their network and plans for growth and profitability.

The question is not whether Tennessee is generally strong for logistics. The question is why this specific business matters in this market.

This is where local knowledge helps. A business with strong regional client relationships, proximity to active freight movement, or established third-party logistics coordination may be more attractive than its financials alone. The point is not to make broad claims about the market. It is to show why this specific logistics business occupies a useful position in Tennessee.

Read Next: Why Exit Planning for Business Owners Prevents Regret and Builds Legacy

Most deals do not weaken because a buyer loses all interest. They weaken because the seller’s claims are harder to support than expected. That usually shows up as slower diligence, lower confidence in management, or pressure on price and terms. If you want to get the highest credible offer, avoid the mistakes that make a logistics business look less transferable or less reliable than it actually is.

Using valuation language without support: Quoting a multiple without showing normalized cash flow, customer concentration, service-line margin, fleet burden, and transfer risk usually makes the seller’s expectations look ungrounded. A buyer will not accept a valuation just because it sounds consistent with the market.

Financial statements that do not reconcile: When internal profit and loss statements do not tie to filed tax returns, monthly balance sheets, payroll records, debt schedules, or aging reports, buyers start questioning the quality of the earnings. That affects both credibility and the price for your business.

Customer relationships that live with the owner: If major freight accounts depend on the owner’s phone, pricing memory, or personal relationship rather than documented account coverage, the buyer sees retention risk under new ownership. That is especially important when a small number of accounts drive a large share of revenue.

Weak support for revenue quality: A logistics business can show strong revenue and still disappoint in the market if the seller cannot break out revenue streams, gross profit by service line, contract terms, renewal patterns, and customer concentration. Buyers are looking for evidence that the business’s cash flow is expected to continue, not just proof that freight moved last year.

Incomplete fleet and maintenance records: Missing VIN schedules, title files, lien payoff detail, maintenance logs, downtime history, or replacement planning can make a truck fleet look riskier than it may actually be. For asset-based operators, buyers often compare those records directly against the company’s claims about operational efficiency and fleet maintenance.

Waiting too long to organize compliance files: Claims runs, insurance renewals, registrations, UCC releases, roadside inspection history, and other regulatory compliance records should be ready before diligence begins. FMCSA’s SAFER system makes crash, inspection, out-of-service, and safety-rating information publicly accessible, so buyers can often review parts of that risk profile independently.

Transition planning that stays too vague: If the seller has not defined how long they will stay, which relationships they will hand off, who will own dispatch or account coverage after closing, and what support is included in the sale process, the buyer has to price that uncertainty into the deal.

Presenting the company as more scalable than it is: Buyers lose confidence when the marketing package suggests a management-driven logistics company, but the facts show that pricing, dispatch, exception handling, customer recovery, or growth still depend on the owner. That gap between presentation and reality can damage the diligence process.

Read Next:

A logistics business usually sells better when the seller prepares for diligence before going to market. This means knowing what the buyer will review, organizing the records that support valuation, and fixing transfer, title, lien, contract, or compliance problems before they affect price and terms. Good preparation does not just make the business look stronger. It reduces avoidable delays, supports a more defensible sale price, and improves the odds of getting to closing without unnecessary concessions.

Prepare The Evidence: Assemble tax returns, monthly statements, top-customer revenue reports, maintenance logs, claims files, and title records before buyer outreach begins so diligence starts from proof instead of cleanup.

Strengthen Transferability: Move relationships, workflows, and daily decisions out of the owner’s head and into documented roles, systems, and management coverage that a buyer can inherit with confidence.

Protect The Deal Early: Define LOI priorities, working capital expectations, contract assignment issues, and transition scope before exclusivity starts so your leverage does not weaken later.

The earlier you test your business the way a buyer will, the more defensible your sale process becomes.

At Legacy Entrepreneurs, we work with Tennessee business owners who need a clearer path through valuation, preparation, buyer screening, negotiation, and closing. Our business valuation support and one-on-one advisory approach help you assess what your logistics company can realistically support in the market and identify what should be addressed before buyer diligence begins.

Request a business valuation to clarify what your logistics company is worth, surface deal risks early, and move toward a cleaner sale process with stronger price support.

That depends on cash flow, customer concentration, fleet condition, claims history, management depth, and how transferable the business is under new ownership. Buyers do not value trucking companies by asset count or revenue alone. They usually start with normalized earnings, then adjust for risk such as major customer dependence, deferred maintenance, or owner-heavy operations. If you want a realistic answer, the valuation should reconcile financial statements, tax returns, equipment obligations, and customer-level revenue rather than rely on a rough industry multiple.

Logistics companies sell transportation and supply chain services, but buyers care about the exact service mix because each one carries a different margin and risk profile. A logistics business may generate revenue from freight brokerage, truck-based hauling, third-party logistics coordination, warehousing support, freight forwarding, intermodal moves, or specialized route management. In a sale process, that mix matters because it affects predictability, customer stickiness, operational complexity, and the type of buyer most likely to pay for the business.

A logistics company should be marketed confidentially, with a well-supported narrative built around strong financial performance, customer satisfaction and quality, operational systems, fleet condition, and transferability. Serious buyers expect a concise opportunity summary first, followed by a stronger confidential information memorandum once they are qualified. The goal is not broad exposure. It is attracting the right buyers with enough evidence to support interest while protecting the business, employees, and customer relationships during the sale process.

The timeline depends on how organized the seller is before going to market, how clean the records are, the strength of buyer demand, and whether financing is involved. A transportation company with reconciled financials, assignable contracts, clean lien records, strong safety files, and low owner dependency typically moves faster than one that still needs documentation cleanup. The process usually slows when buyers find unclear add-backs, unresolved equipment liens, weak customer transferability, or insurance and claims issues that require deeper diligence.

You do not legally need a business broker, but a broker can help structure valuation, prepare materials, qualify buyers, protect confidentiality, and manage the diligence process with more discipline. In logistics, that matters because the transaction often includes customer concentration analysis, fleet and lien review, safety and claims scrutiny, working capital issues, and contract transfer questions that can change deal terms. A broker with Tennessee market knowledge can also help position the business with more relevant buyers and reduce preventable process mistakes.

Buyers usually ask for tax returns, monthly financial statements, trailing twelve-month performance, debt schedules, top-customer revenue reports, customer contracts, fleet schedules, maintenance files, insurance policies, claims runs, title records, UCC information, and key compliance records. They use these documents to verify cash flow, transferability, capex risk, contract durability, and whether the business can continue operating smoothly after acquisition. Missing or inconsistent records almost always slow diligence and weaken confidence.

Your roofing company's sale price comes down to one question a buyer is always asking: how much money will this business make me, and how confident...

SDE stands for Seller's Discretionary Earnings. It is the total financial benefit a single owner-operator receives from a business in a year. It...

Private equity is buying roofing companies because the industry has exactly what investors want: huge size, heavy fragmentation, and demand that does...