Asset Sale vs. Stock Sale: Why the Structure Matters as Much as the Price

An asset sale and a stock sale can lead to very different outcomes for a business owner. In most Tennessee business transactions, buyers prefer asset...

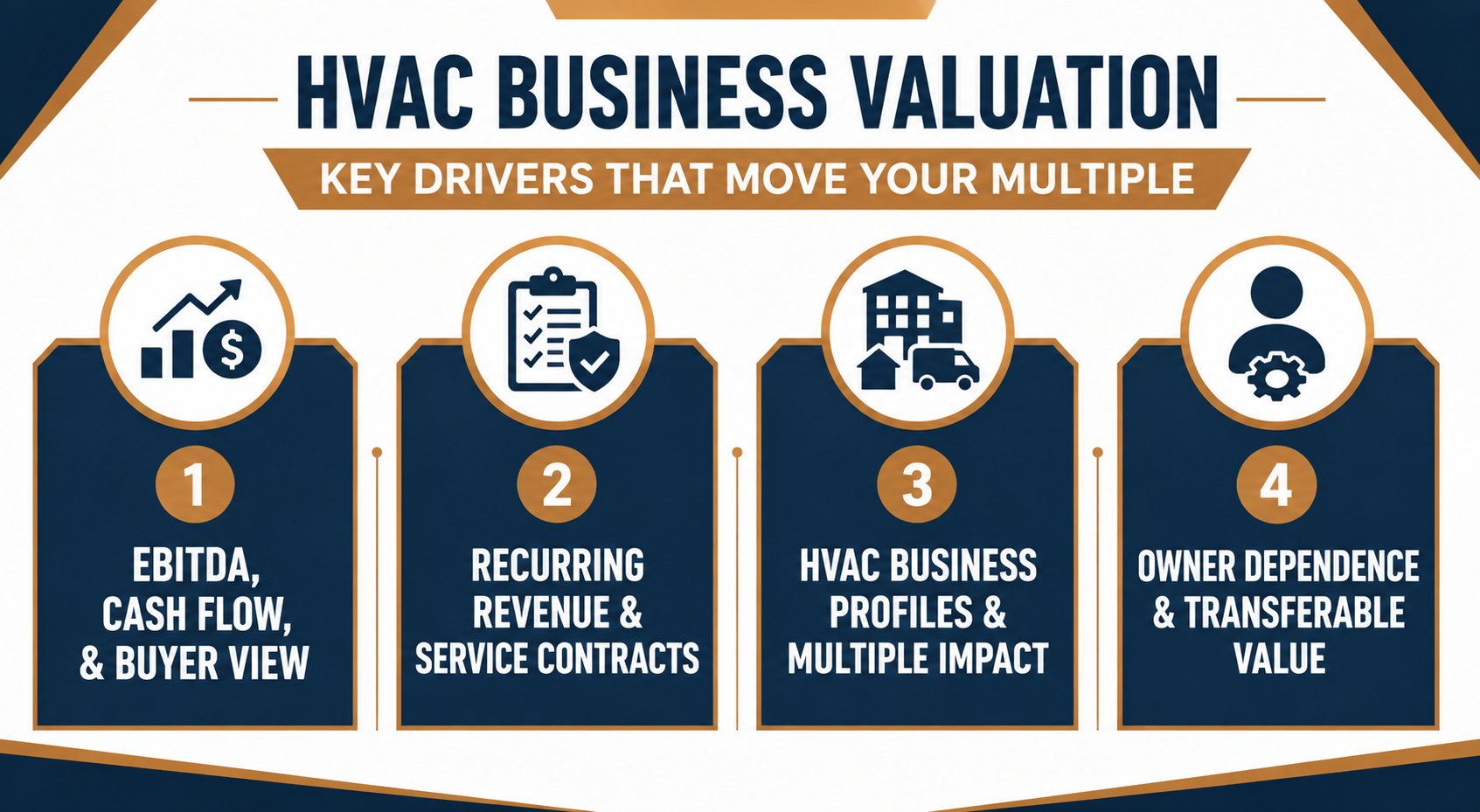

The value of your HVAC business in Tennessee depends less on revenue size and more on recurring revenue, clean EBITDA, and how well your business runs without you. Buyers want to understand whether the company has recurring maintenance agreements, clean and defensible EBITDA, reliable technicians, documented systems, and a customer base that will remain after the owner steps away.

Many business owners enter a sale process with a price in mind, but buyers look for proof behind the number. In KPMG’s 2024 U.S. M&A Deal Market Study, 37% of dealmakers said high valuation expectations prevented them from moving forward on potential targets, and 26% cited unfavorable diligence findings.

Valuation is not just about what the company earns today. It is also about how clearly the business can prove its earnings, reduce buyer risk, and show that future cash flow is sustainable.

This guide covers:

How HVAC buyers in Tennessee evaluate businesses and why demand has stayed strong post-2020.

The valuation drivers that move EBITDA multiples up or down for different HVAC business types.

Practical steps to prepare your financials, service contracts, and operations for buyer due diligence.

When to involve a Tennessee HVAC business broker to protect confidentiality and maximize your sale.

Buyer demand in Tennessee for residential and commercial HVAC companies with recurring revenue streams remains high.

Multiples are driven less by revenue size and more by clean EBITDA and contract quality.

Service and maintenance contracts plus commercial accounts tend to command higher multiples than one-off installs.

Clean, SBA-ready financial records, including tax returns, P&Ls, depreciation, and amortization, are non-negotiable for top buyers.

Owner-dependent HVAC shops usually need a strong number-two or GM to reach maximum value.

Due diligence will test your customer base, recurring revenue, and operational efficiency, not just top line.

A Tennessee-focused business broker can protect confidentiality, find the right buyer, and structure a successful sale.

HVAC is attractive because it's essential and non-discretionary. Residential and commercial HVAC demand stays steady across economic cycles. Maintenance contracts and service agreements create recurring revenue streams that reduce buyer risk.

Growing Tennessee markets like Nashville and Middle Tennessee generate strong local search and referral-driven demand. High demand does not mean every HVAC company gets the same multiple. It increases the pool of serious buyers if your fundamentals are strong.

Different buyer types prioritize different strengths in an HVAC business.

A Tennessee-focused business broker who regularly speaks with all three buyer types can pre-screen who's looking for businesses like yours and orchestrate quiet outreach while protecting confidentiality. Legacy ETA works one-on-one with HVAC business owners across Tennessee, connecting them with serious buyers who fit their business profile, deal structure, and transition goals.

HVAC business valuation starts with earnings before interest, taxes, depreciation, and amortization—EBITDA—and applies a multiple based on risk, recurring revenue, customer base quality, and operational transferability. Buyers look at normalized EBITDA, which means they adjust for owner salary add-backs, personal expenses, and one-time costs to understand what the business actually earns. The multiple applied to that EBITDA depends on how predictable the cash flow is, how dependent the business is on the owner, and how much of the revenue comes from recurring service contracts versus one-off installs or new construction.

EBITDA is the starting point for most HVAC business valuations. Buyers want to see what the business earns before financing costs, tax structure, and accounting decisions. They normalize EBITDA by adding back the owner's salary to market rate, removing personal expenses run through the business, and adjusting for one-time costs like equipment purchases or facility repairs. This gives them a clear picture of what your business is worth as a cash-flowing asset.

Clean financial records and tax returns covering at least three years directly impact the buyer pool. Most small business owners rely on SBA loans to finance acquisitions. SBA lenders require reconciled financials, clear depreciation schedules, and tax returns that match your P&Ls.

If your books are inconsistent, show unexplained cash, or don't reconcile to your tax returns, you lose access to SBA-backed buyers and reduce your selling price. Business valuations that account for these adjustments give you a realistic view of what buyers will actually pay.

Service contracts and maintenance agreements are the most valuable revenue streams in an HVAC business. Buyers see recurring revenue as lower risk because it's predictable and less dependent on seasonal demand or one-off sales.

Residential service contracts spread across many households create a stable base. Commercial accounts with property managers, small chains, or repeat maintenance agreements are often seen as higher-quality revenue because they renew annually and generate consistent cash flow.

HVAC companies that rely heavily on new construction or one-off installs face more volatility. New construction revenue is cyclical and tied to housing starts and commercial development. One-off service calls generate larger spikes in cash flow but don't create the predictable revenue base that commands higher multiples.

Buyers pay more for businesses where 30% or more of revenue comes from recurring service contracts and maintenance agreements. If your business is install-heavy, building a maintenance contract based on 12 to 24 months can meaningfully increase your business value before you sell.

Different types of HVAC businesses command different multiples based on revenue mix, owner dependence, and risk profile.

This is directional, not a promise. Companies are valued based on exact numbers, financials, and risk. Owners can often move from one profile toward a more attractive one over one to three years by building service contracts, hiring a GM, and cleaning up bookkeeping. Small improvements in recurring revenue, financial documentation, and operational independence can shift your business from the bottom row to the middle or top row of this table.

Recurring revenue, operational independence, and service contract stability directly influence buyer risk perception. HVAC businesses with diversified revenue, lower owner dependence, and established maintenance agreements typically receive stronger valuation multiples than companies heavily tied to new construction or a single owner-operator.

Owner dependence is one of the most common valuation drags in HVAC businesses. When the owner handles all estimating, manages key customer relationships, and makes every operational decision, buyers see a business that can't transfer cleanly. Reducing that dependence by building a capable team or hiring a general manager directly increases what buyers will pay.

Why owner dependence is a valuation drag. Buyers worry when all estimating, key customer relationships, and operational decisions run through one HVAC contractor. If you're the only person who can price jobs, manage commercial accounts, or handle dispatch, the business is not transferable. That increases buyer risk and lowers the multiple.

How a strong number-two or GM changes the story. A capable general manager or operations lead improves transferability and can support a higher sale price. Buyers see a GM-led HVAC company as lower risk because the business can operate without the owner. That makes the business more attractive to strategic buyers and easier to finance through SBA loans.

What small business owners can realistically build in 12 to 24 months. Document processes, delegate dispatch and estimating, and gradually move into a strategic role. You don't need to disappear from the business, but you do need to show that the business can run without you making every decision.

Why Tennessee buyers favor GM-led HVAC companies. It reduces transition risk and makes SBA lenders more comfortable with the cash flow. A business that depends entirely on the owner is harder to finance and harder to sell.

Read Next: Guide to Hiring a General Manager

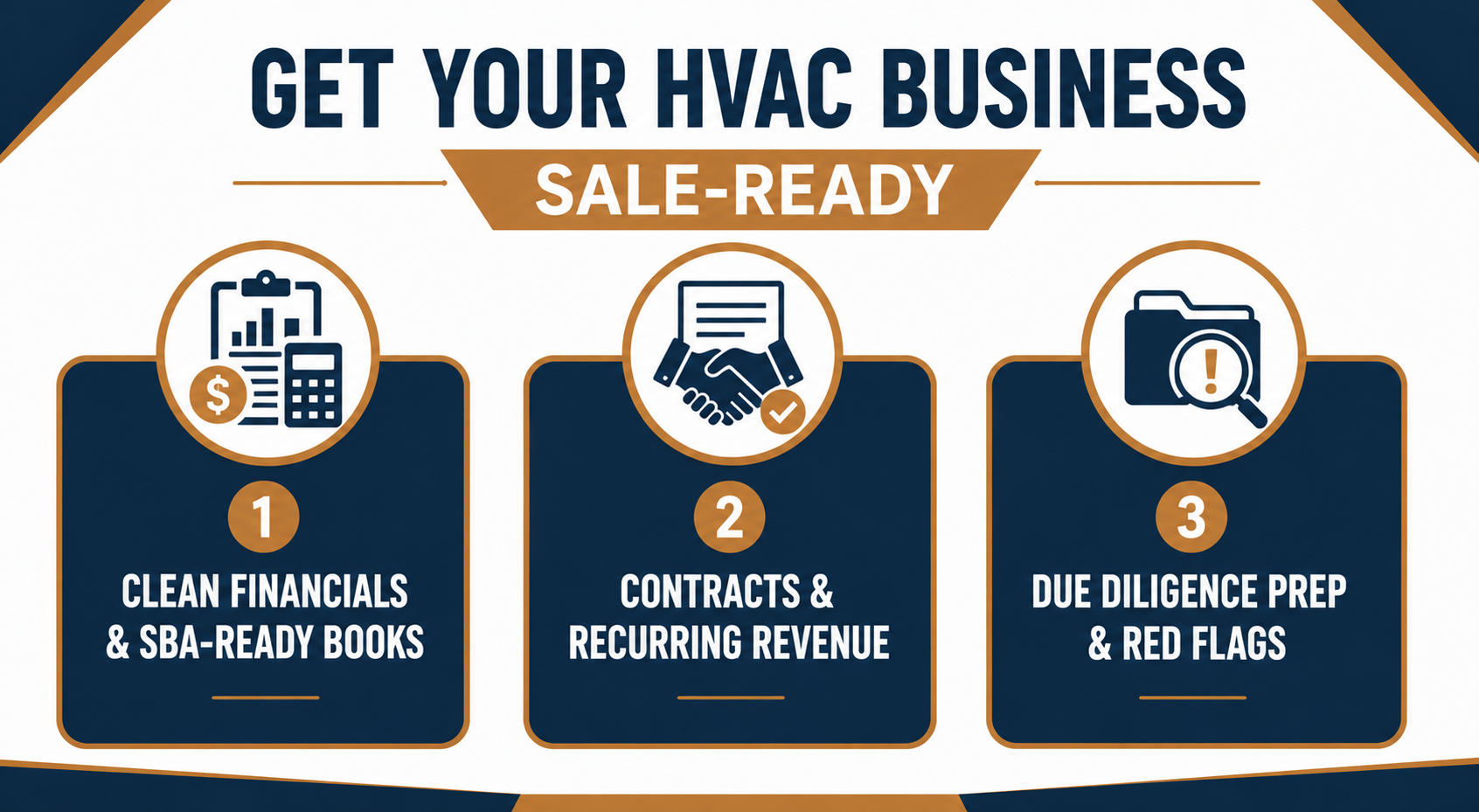

Preparation is the first step in increasing your business value, once you start to seriously consider selling your HVAC company. Buyers and SBA lenders will test your financial records, service contracts, customer base, and operational documentation during due diligence. Small improvements in these areas can meaningfully impact your sale price and reduce the risk of deals falling apart during the business sale process.

Clean, accrual-based financial records and reconciled accounts are non-negotiable for serious buyers. Most buyers rely on SBA loans to finance small business acquisitions. SBA lenders require three to five years of tax returns, reconciled P&Ls, clear depreciation and amortization schedules, and equipment lists. If your books are cash-basis, inconsistent, or don't match your tax returns, you lose access to the largest pool of buyers.

Poor bookkeeping, unexplained cash deposits, or inconsistent financials can tank your multiple and delay or kill deals. Buyers assume that messy books hide problems. Even if your business is profitable, unclear financial records create doubt. Cleaning up your books six to twelve months before you list gives you time to reconcile accounts, document add-backs, and present financials that support your asking price.

Buyers will scrutinize your service contracts, customer base, and recurring revenue during due diligence. Verbal agreements and informal maintenance arrangements don't count as recurring revenue in a buyer's eyes. Formalizing these relationships into written contracts and organizing your customer data makes your HVAC business more valuable and easier to sell.

Service and maintenance contracts. Formalize what's currently handshake agreements into written contracts with clear terms and renewal structures. Buyers want to see signed maintenance agreements, not verbal commitments. Written contracts are recurring revenue. Verbal agreements are not.

Customer base concentration. Identify whether a few commercial accounts drive too much revenue and how that appears in due diligence. If one or two customers represent 30% or more of your revenue, buyers see concentration risk. Diversifying your customer base before you sell reduces that risk and supports a higher multiple.

Home services recurring revenue. Create simple, trackable residential maintenance plans that can be shown to buyers as recurring revenue streams. Annual HVAC tune-ups, filter replacement programs, and priority service memberships are all recurring revenue that buyers value.

Documentation buyers and lenders expect. Contract copies, lists of maintenance agreements, renewal rates, and payment histories. Buyers will ask for this during due diligence. Having it organized upfront speeds the process and builds buyer confidence.

Buyers and lenders will scrutinize every part of your business during due diligence. The table below shows what raises red flags versus what positions your HVAC business as sale-ready.

Small improvements here can meaningfully impact your sale price and maximum value. Most HVAC owners underestimate the amount of documentation buyers, banks, and due diligence teams will expect. Starting this prep six to twelve months before you list gives you time to fix gaps without rushing.

The business sale process for an HVAC company typically takes several months. Working with a Tennessee business broker who understands HVAC operations, home services buyers, and SBA financing protects your confidentiality, screens out unqualified buyers, and structures a deal that protects your interests.

The sale process follows a structured path from initial valuation through closing. Each step protects your confidentiality, qualifies buyers, and positions your HVAC business to command the best terms. Understanding this timeline helps you plan when to start and what to expect at each stage.

Initial consultation and confidential valuation. Establish what your HVAC business is worth today and what buyers will see. This includes a market-based valuation, a review of your financials, and a discussion of timing and readiness.

Preparation and packaging. Clean up financials, organize service contracts, and build a strong, confidential information memorandum. This document presents your business to buyers without revealing your identity until they've signed a non-disclosure agreement.

Quiet marketing and buyer outreach. Approach strategic buyers, HVAC companies, and investment groups without public "business for sale" listings. Confidentiality is critical. You don't want employees, customers, or competitors to know you're selling until you have a signed letter of intent.

Offers, LOIs, and negotiation. Evaluate offers beyond just price—terms, SBA structure, employment and transition expectations, and risk allocation. A higher offer with bad terms can be worse than a lower offer with a clean structure.

Due diligence and closing. Navigate financial, operational, and legal review without disrupting your successful HVAC business. Buyers will verify everything you've represented. Having clean documentation from the start makes this phase faster and less stressful.

Working with a Tennessee-based business brokerage like Legacy ETA, which knows the local market, buying appetite, and SBA lender expectations, gives HVAC owners an advantage over purely national brokers. You work one-on-one with a seasoned advisor who understands Nashville and Middle Tennessee growth, HVAC industry dynamics, and the operational realities of home services businesses.

There are no handoffs. You're not passed to a junior associate halfway through the process. Legacy ETA's model is built around deep practice in guiding small business owners who are selling for the first time through a complex, high-stakes transaction.

Read Next: Guide to Selling Your Business

A successful HVAC business is not automatically a sale-ready asset. Timing, preparation, and the right support can transform years of work into a meaningful, lower-stress exit. Buyer demand for HVAC businesses in Tennessee remains strong, but the businesses that command top dollar are the ones with recurring revenue, clean EBITDA, transferable operations, and documentation that survives due diligence.

Understand what really drives HVAC valuation. Recurring revenue, clean EBITDA, and transferability usually matter more than raw revenue.

Treat preparation like a project. Clean books, contract documentation, and a capable team protect your sale price and reduce due diligence pain.

Choose a Tennessee partner who knows home services. The right broker and valuation advisor can help you maximize your sale and protect your legacy.

Legacy ETA is a Tennessee business brokerage and advisory firm that works closely with home services owners—HVAC, roofing, and other trades—who are considering selling or building a more sellable business over time. Our home-services operational insight, including programs for roofing GM hiring, and lead infrastructure, maps directly onto HVAC companies looking to work out owner dependence, recurring revenue gaps, and exit readiness.

Schedule a confidential business review to understand your HVAC company's market value and plan your next move.

HVAC businesses are valued based on normalized EBITDA multiplied by a multiple that reflects recurring revenue, owner dependence, and risk. Service-heavy HVAC companies with strong maintenance contracts and low owner dependence typically command multiples between 4x and 8x EBITDA. New-construction-heavy or owner-dependent businesses often see lower multiples. Clean financials, commercial accounts, and a capable GM can push your multiple higher.

Buyers and SBA lenders expect three to five years of tax returns, reconciled profit-and-loss statements, balance sheets, depreciation and amortization schedules, and equipment lists. Your financials must match your tax returns. Inconsistent books, unexplained cash, or missing documentation will delay or kill deals. Clean, accrual-based records are non-negotiable for serious buyers.

Service contracts and maintenance agreements create recurring revenue, which reduces buyer risk and commands higher multiples. HVAC businesses where 30% or more of revenue comes from recurring contracts typically see multiples one to two points higher than install-heavy businesses. Buyers pay more for predictable cash flow.

Hiring a general manager before you sell reduces owner dependence and increases business value. Buyers see GM-led HVAC companies as lower risk and easier to finance. If your business depends entirely on you for estimating, customer relationships, and operations, hiring a GM 12 to 24 months before you sell can meaningfully increase your sale price.

The business sale process typically takes six to twelve months from initial valuation to closing. Preparation, buyer outreach, negotiation, and due diligence all take time. Businesses with clean financials, strong contracts, and transferable operations tend to sell faster. Owner-dependent businesses or those with messy books take longer.

A Tennessee HVAC business broker manages confidentiality by using non-disclosure agreements, approaching buyers quietly without public listings, and controlling who sees your business information. Employees, customers, and competitors should not know you're selling until you have a signed letter of intent. Confidentiality protects your business value and prevents disruption.

The most common buyers are strategic HVAC contractors expanding into new territories, home services groups and private equity firms building platforms, and individual operators looking for stable, cash-flowing businesses. Each buyer type values different strengths. Strategic buyers want service contracts and commercial accounts. PE firms want recurring revenue and scalable systems. Individual operators want turnkey teams and simple structures.

The right time to consider selling is when you're ready to transition to your next chapter and your business is positioned to command maximum value. If your financials are clean, you have recurring revenue, and your business can operate without you, you're ready to sell. If not, spending 12 to 24 months building contracts, hiring a GM, and cleaning up books can significantly increase your sale price.

An asset sale and a stock sale can lead to very different outcomes for a business owner. In most Tennessee business transactions, buyers prefer asset...

If you're thinking about selling a manufacturing business in Tennessee, valuation and buyer interest are largely driven by cash flow, customer...

A successful restaurant exit starts long before you put the business on the market. Whether you own an independent restaurant, a restaurant...