5 Things That Actually Drive Your Roofing Company's Sale Price (and 3 That Don't)

Your roofing company's sale price comes down to one question a buyer is always asking: how much money will this business make me, and how confident...

The real decision is not whether you can list a business next month. It is whether your financials, valuation, lease terms, and transfer documents can hold up long enough to get from buyer interest to closing. Most delays happen after a business owner thinks the hard part is done, because a potential buyer, lender, landlord, or attorney starts asking for records that should have been prepared before the business ever went to market.

That timing pressure matters because many owners are counting on the proceeds from the sale to fund retirement, reduce burnout, or move into a different role. Gallup research found that 74% of small business owners with employees say they plan to sell or transfer ownership of their business when they retire, which makes timeline mistakes expensive, not just inconvenient.

This guide covers

How long does each stage of a Tennessee business sale usually take

What documents, approvals, and buyer checks slow deals down

Steps that shorten delays and improve closing credibility

P.S. Before you list a business for sale, it helps to know whether the valuation, financial statements, legal documents, and transfer terms will hold up once a buyer starts reviewing the acquisition.

At Legacy Entrepreneurs, we help Tennessee business owners prepare to sell a business through our business brokerage support and business valuation services built around readiness, pricing discipline, and buyer confidence.

Contact a broker today to identify timeline risks, document gaps, and transfer issues before they slow the sale of your business.

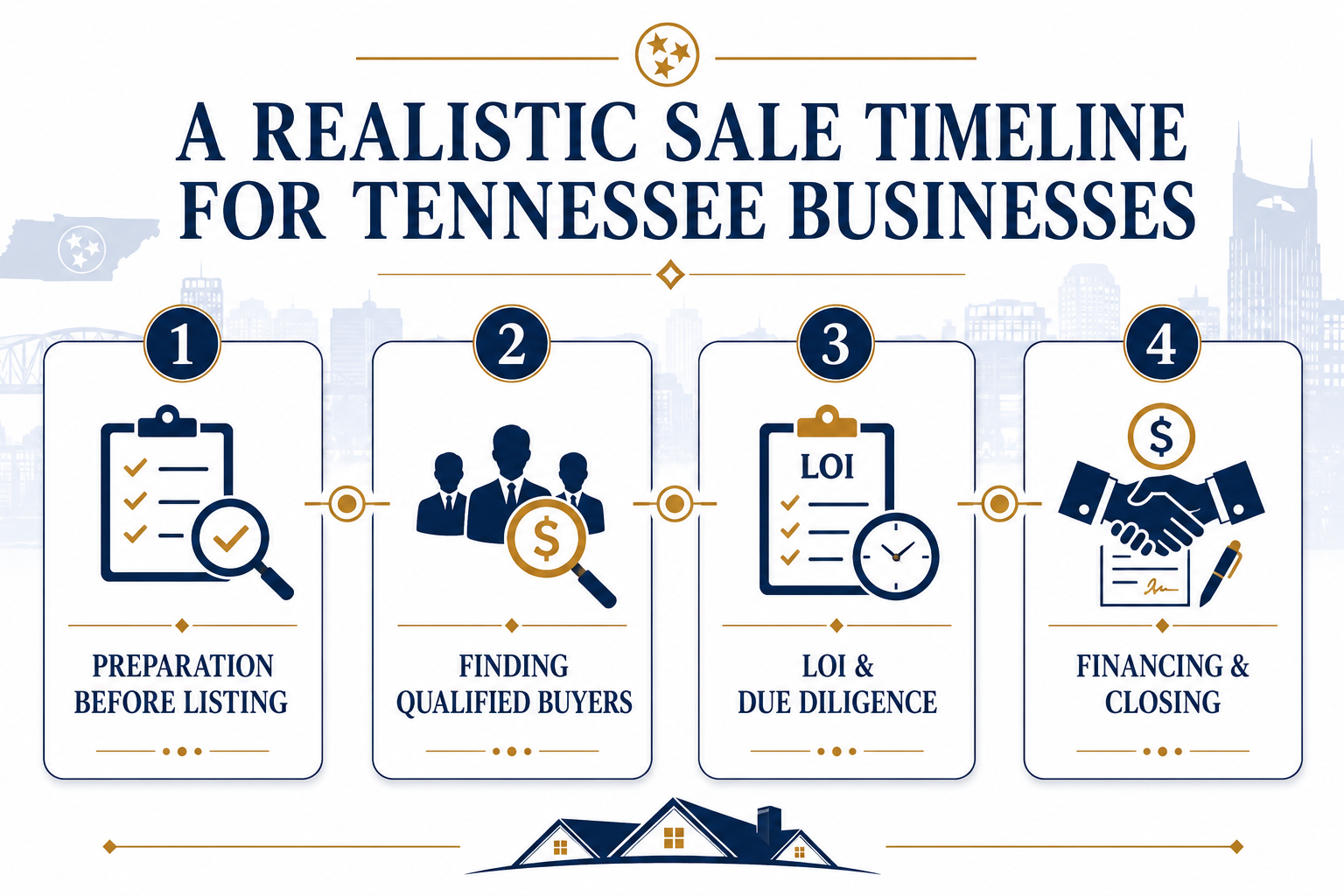

The answer depends on the type of business, the size of the business, the quality of the financials, and how ready the business owner is before the sales process starts. Many business owners think the time to sell a business begins when the listing goes live. In practice, the time it takes to sell often starts earlier, with valuation work, legal cleanup, lease review, and document preparation that determine whether a buyer can move from interest to a signed agreement.

Legacy Entrepreneurs’ position is clear: six months is fast. That is why a broker may ask for 12 months of exclusivity even when the owner wants to move quickly. The reason is practical. Even a clean process usually requires one month of marketing prep, at least one month to find buyers and get offers, and at least one month of due diligence, which means three months is the minimum if everything is ready on day one. A more common path is one month of prep, two months of sourcing buyers and letting them complete pre-LOI screening, and another month of diligence. If diligence fails, the business goes back to market.

The fastest version of a business sale is not the normal one. A buyer still has to be found, screened, and moved through confidentiality controls before serious offers appear. Then the buyer has to verify the numbers, contracts, and legal transfer rights. That is why the time it takes to sell is controlled by stages, not by a single headline number.

A professional business sale starts with records, not marketing. A business broker can help organize the process, but the seller still needs to produce the evidence that supports value and transferability. Without that, the time to sell stretches before a buyer even appears.

Legacy Entrepreneurs believes it can even take three years of preparation to start selling, even if many businesses only need about one month of prep. That prep period is part of the real timeline. If the business owner skips it and rushes to market, the likely result is a weaker valuation, a slower buyer process, or failed diligence after a buyer is already under agreement.

Financial Statements: Prepare monthly and annual financial statements that tie to bank activity and filed tax returns so the buyer can test financial performance and cash flow instead of debating basic credibility.

Tax Returns: Organize at least three years of tax returns because lenders and buyers use them to verify earnings quality, compare trends, and conduct due diligence to verify whether the internal books tell the same story.

Business Valuation Support: Build a grounded business valuation with adjusted earnings, support for add-backs, and an explanation of unusual periods so the sale price reflects reality and helps you negotiate from a position of credibility.

Lease Review: Pull the full lease, amendments, assignment language, years remaining, renewal options, and rent escalations because the lease can determine whether the business would likely sell at the expected purchase price.

Legal Documents: Assemble operating agreements, bylaws, permits, licenses, debt schedules, equipment leases, and entity records so the sale of a business does not stall over missing authority or unresolved obligations.

Owner Dependency Review: Identify what the business owner still controls personally, such as key sales, hiring, major vendor decisions, or customer relationships, because businesses that only run through the owner are harder to sell.

Confidential Information Package: Prepare clear confidential information that explains revenue, margins, staffing, customers, supplier relationships, and growth potential without exposing the business prematurely to the market.

Many business owners make the mistake of assuming prep is optional if they want to sell quickly. In reality, that prep work is part of the time it takes. Skipping it often adds more delay later, when a potential buyer has already started asking harder questions.

Finding a buyer is not the same as finding the right buyer. Most inquiries do not come from qualified buyers. They come from interested parties who are curious, undercapitalized, inexperienced, or not ready for the acquisition process.

It can take one month to find buyers and get offers, but it's only possible in a cleaner, faster process. However, many deals take closer to two months because buyers need time for pre-LOI screening.

A business brokerage process should protect confidentiality from day one. Employees, customers, and suppliers should not learn that the business is for sale from a loose conversation or broad ad copy. The broker needs a confidentiality agreement, screening steps, and a way to separate casual inquiries from buyers who can actually review confidential information responsibly.

A broker also needs to assess whether the potential buyer has funds, lender access, industry fit, and enough operational understanding to run the business after closing.

The Tennessee market affects this stage, too. Some local business opportunities attract first-time buyers, strategic acquirers, or private equity interest because the cash flow is stable and the transfer is straightforward. Others tend to sell more slowly because the type of business is specialized, regulated, seasonal, or too dependent on one owner. That is one reason business owners think exposure alone will solve the timeline. It will not. The quality of the buyer pool matters far more than the volume of attention.

Many business owners get excited when they receive an LOI, but the time for the buyer often becomes more demanding after exclusivity begins. The LOI is not the purchase agreement. It is the starting point for deeper verification.

Financial Review: The buyer will compare financial statements, tax returns, bank support, balance sheets, and margin trends to test whether the business valuation and asking price still hold up.

Cash Flow Analysis: Buyers want to know whether the cash flow is recurring, whether owner add-backs are real, and whether the business can run after closing without hidden labor or management costs.

Purchase Agreement Drafting: Attorneys turn the LOI into a purchase agreement that covers assets included, excluded liabilities, indemnity terms, transition support, non-compete language, and conditions to closing.

Lender Underwriting: Financing for a small business often requires lender-ready records, lease review, debt payoff detail, and entity documents, which can slow the process even when the buyer remains committed.

Third-Party Consents: Lease assignment, key customer approvals, supplier notices, and franchisor or licensor consent may all be required before the agreement can close.

Working Capital and Structure Review: The buyer may revisit whether the purchase price should stay the same once inventory, payables, accrued expenses, and required working capital are reviewed in detail.

This is where the length of time it takes to sell a business becomes a live issue rather than a planning estimate. Diligence and financing are the stages that prove whether the business can support the original deal. If the evidence is weak, the purchase price drops, the buyer asks for better terms, or the transaction dies.

A signed LOI does not mean the sale of your business is secure. Diligence can fail, financing can fail, and legal transfer issues can derail a deal after weeks of work. When that happens, the business goes back to market, and the timeline resets.

Financial credibility is the most common reason. The buyer may discover that internal books do not match tax returns, that margins are weaker than expected, or that personal expenses were mixed into the business without support. The same problem appears when cash flow depends on the owner more than the marketing materials suggest. A buyer who cannot trust the numbers will either renegotiate the purchase price or leave.

Transferability failures are just as serious. A landlord may not approve an assignment. A supplier may not continue the terms. A license may require a new application rather than a simple transfer. A contract may contain change-of-control restrictions. If those issues were ignored early, the business selling process becomes slower, more expensive, and less credible with the next round of buyers.

That is why many business owners should plan around the possibility that one diligence cycle may not close. This is not a house transaction. A sale of a business involves earnings verification, legal rights, tax exposure, operational continuity, and post-closing risk that the buyer has to evaluate in detail.

A faster transaction usually means fewer unknowns. It does not mean the broker got lucky. It means the business was easier to understand, easier to finance, and easier to transfer.

Grounded Asking Price: A realistic asking price tied to adjusted cash flow, market conditions, and transferability attracts qualified buyers instead of pushing them away.

Clean Financial Performance: Stable revenue, explainable margins, and organized financial statements reduce friction during due diligence and lender review.

Strong Transferability: A business can run with managers, documented systems, and less dependence on the owner, which makes the acquisition easier for the buyer to underwrite.

Clear Lease And Contract Position: Assignable lease terms, manageable supplier relationships, and customer contracts with limited consent problems make closing the deal more predictable.

Buyer Readiness: A potential buyer with proof of funds, lender access, and realistic expectations can move far faster than casual prospective buyers still exploring the market.

Responsive Advisors: Sellers who use the services of a professional broker, CPA, and attorney early usually speed up the process because document requests and agreement revisions move faster.

Longer transactions usually show the same problems. These are the issues that make a small business harder to sell, reduce buyer confidence, and increase the average time to sell.

Weak Bookkeeping: Bad records, inconsistent financial statements, and unsupported adjustments make it difficult for the buyer to confirm the purchase price.

Inflated Sale Price: Many business owners think the market will validate a number based on personal goals, but an unrealistic sale price slows buyer response and weakens negotiation leverage.

Heavy Owner Dependence: If the owner still runs the business personally, manages all key decisions, and owns the customer relationships, the buyer sees transition risk.

Limited Growth Potential: If the business also shows flat demand, weak systems, or no path to maintain performance after the owner exits, qualified buyers become harder to attract.

Compliance Problems: Missing permits, unresolved state tax issues, legal documents that are out of date, or contract assignment problems create real closing risk.

Narrow Buyer Pool: Some businesses tend to sell slowly because the type of business is specialized, the location is limited, or lenders do not like the sector.

Failed Diligence Cycle: Once a deal breaks, the next buyer asks why. That alone can take anywhere from a few extra weeks to several months to overcome, depending on what failed.

Read Next: Top 3 Reasons Business Owners Leave Money on the Table When Selling Their Business

Tennessee-specific legal, tax, and licensing issues can slow a sale even when the buyer is serious, and the price is already negotiated. Buyers, lenders, and counsel often need to confirm that the business is in good standing, that required tax accounts and filings are current, and that any required licenses or permits can remain in place or be updated after closing.

These issues matter because owners often assume delays come from the market or from financing alone. In practice, timing problems often come from internal cleanup items such as missing authority documents, unresolved tax registrations, or approvals tied to the current owner, entity, or location.

In Tennessee, the right review usually depends on the company’s structure and industry. A restaurant, contractor, or other regulated business may face a different transfer process than a standard service company, which is why these issues should be reviewed before the business is listed.

Before you sell your business, the entity should show clear authority to complete the transaction. For an LLC or corporation, buyers and counsel will typically want to review governing documents, ownership records, and approval authority, and they may also check the company’s Tennessee business record and good-standing status.

This matters because ownership disputes, outdated records, or missing approvals can delay drafting and signing even after the business terms are settled. The legal structure also affects the deal itself, since many small business transactions are structured as asset sales, which means the parties need to identify exactly which assets, contracts, permits, and liabilities will or will not move at closing. This transaction-structure point is common deal practice rather than a Tennessee-only rule, so it is safest to present it that way.

Tax cleanup often decides whether diligence moves cleanly or drags.

They play a direct role in buyer diligence, lender review, and overall closing preparation because they help confirm how the business has been reporting income, handling tax obligations, and maintaining compliance over time. In Tennessee, they also matter at the end of the process, since businesses that close or cease operations may need to submit final state filings and resolve open tax accounts before the transaction is fully wrapped up.

Tax Returns: Provide at least three years of filed tax returns and make sure they reconcile to internal financial statements so the buyer can test performance with confidence. This is a diligence best practice rather than a Tennessee-specific filing rule.

State Tax Accounts: Review Tennessee tax registrations, notices, and account status early because unresolved issues can delay diligence and create extra closing work. Tennessee requires businesses to register for applicable taxes through TNTAP, and businesses that close must file final returns where required.

Sales and Use Tax Exposure: Confirm that taxable sales, exemptions, and remittances were handled correctly where applicable. Tennessee requires sales and use tax registration for businesses making taxable sales, and account cleanup is easier before the closing process intensifies.

Payroll Filings: Check payroll tax records and worker classification with your tax advisors because labor and payroll issues often become diligence problems. This is good transaction practice, though the exact review may involve federal and multistate issues beyond Tennessee-specific rules.

Debt And Lien Records: Organize payoff information, UCC filings, and debt schedules so the buyer understands what must be released or paid at closing. This is a general closing-readiness point rather than a Tennessee-only requirement.

Purchase Price Allocation: Work with tax advisors on how the purchase price may be allocated across goodwill, equipment, inventory, and other assets because that can affect taxes and net sale proceeds. This is a transaction tax issue, not a Tennessee-specific licensing rule.

License transferability can change the whole timeline. Some approvals move with the entity, some require notice, and some require a new application before the buyer can fully operate. That affects both the time to sell and the buyer’s willingness to sign an agreement at the expected value.

A buyer is not just buying assets. They are buying continuity of operations, rights to occupy the location, customer relationships, and supplier access, so any consent or assignment issue can lengthen the sale process. This is not uniquely Tennessee-specific, but it is still one of the most common reasons a deal slows down late in the process.

Lease Assignment Language: Review assignment clauses, consent rights, years remaining, renewal options, rent escalations, and guaranty terms because the lease often affects value and financing.

Landlord Approval: Understand what the landlord requires, how long approval may take, and whether the landlord has discretion to reject the buyer.

Customer Contract Transfer: Identify major contracts that require consent or contain change-of-control restrictions because revenue continuity can affect the purchase price.

Supplier Agreements: Check whether supplier terms continue after closing or depend on the seller’s relationship, credit, or historical buying volume.

Equipment And Service Contracts: Confirm which agreements must be assigned, paid off, or terminated to avoid last-minute surprises.

Franchise Or Brand Restrictions: Review transfer fees, buyer qualification standards, and approval requirements early if the business operates under a franchise or licensed brand.

Read Next: The Ultimate Guide to Choosing a Business Broker in Tennessee

You cannot control the buyer's decision, but there are steps you can take to reduce avoidable delay. The goal is not to force a rushed deal. The goal is to make the business easier to evaluate, finance, and transfer.

Prepare A Diligence File: Organize financial statements, tax returns, balance sheets, payroll records, lease documents, legal documents, and debt schedules before listing your business.

Build A Defensible Valuation: Use a realistic business valuation supported by cash flow, market logic, and risk factors so you do not lose months defending an inflated asking price.

Review Transferability Early: Check leases, licenses, permits, customer contracts, supplier agreements, and other confidential information points that can affect assignment or consent.

Reduce Owner Dependence: Shift approvals, relationships, and operating knowledge into documented systems so the business can run without daily owner control.

Prepare For Buyer Questions: Be ready to explain revenue swings, margins, staffing changes, concentration risk, and growth potential using evidence rather than general statements.

Use A Disciplined Process: A broker, business advisor, CPA, and attorney working early can help manage confidentiality, buyer screening, agreement flow, and timeline discipline.

Read Next: Bad Bookkeeping Kills Deals — Focus on These 4 Fixes

Owners who want to sell quickly often focus on the first buyer conversation. The stronger approach is to focus on what will still hold up thirty or sixty days later, when the business is under agreement, and every assumption is being tested. That is where the real time it takes to sell is decided.

Treat Three Months As The Floor: Three months is the minimum only when the business is fully prepared on day one, and the buyer process moves unusually cleanly.

Treat Six Months As Fast: Six months is a fast result in this market, not the baseline expectation for the average small business owner.

Treat Exclusivity As Process Protection: A 12-month exclusivity period reflects the reality that buyer sourcing, pre-LOI screening, diligence, financing, and failed deal risk can all extend the timeline.

That is why a disciplined sales process matters more than a short estimate.

At Legacy Entrepreneurs, we work with Tennessee business owners considering selling their business but need a clearer path. We focus on helping business owners get realistic on value, prepare confidential information for qualified buyers, and address transfer risks before due diligence starts.

Contact a broker today to clarify your sale timeline, reduce avoidable deal risk, and move toward a cleaner, more defensible process.

The average time to sell a small business is often several months, with many deals landing in the six to twelve-month range once active preparation, buyer sourcing, due diligence, and closing are included. A clean, well-priced business can move faster. A business with weak financials, lease issues, or financing challenges will often take longer.

Due diligence often takes four to eight weeks in a small business transaction, but it can take longer if the buyer is using lender financing or if the records are incomplete. The buyer and advisors will review financial statements, tax returns, contracts, legal documents, and operating details to verify that the business can support the proposed purchase price.

It is usually time to sell when your goals, financial performance, and transferability are aligned. If the business can run with less owner involvement, the financials are organized, and the valuation is grounded in real cash flow, you are in a stronger position to go to market.

Sales alone do not determine value. Buyers look at cash flow, margins, owner dependence, growth potential, legal and compliance risk, and how easily the business can transfer. Two companies with the same revenue can have very different values if one is easier to operate, verify, and finance.

The first step is to determine whether the business is actually ready to sell. That means reviewing valuation, financials, legal documents, lease terms, tax returns, and transfer issues before marketing begins. Without that groundwork, the sales process often becomes slower and more fragile.

You do not have to use a business broker, but many sellers do because the process involves confidentiality, buyer screening, valuation positioning, due diligence coordination, and agreement management. A broker can help protect the process from unqualified buyers and reduce avoidable delays.

Your roofing company's sale price comes down to one question a buyer is always asking: how much money will this business make me, and how confident...

SDE stands for Seller's Discretionary Earnings. It is the total financial benefit a single owner-operator receives from a business in a year. It...

Private equity is buying roofing companies because the industry has exactly what investors want: huge size, heavy fragmentation, and demand that does...